Saving for Your First Home: 6 Practical Tips

Saving for your first home? Here are six practical tips to be one step closer to buying your dream home.

Owning a home is one of our ultimate goals in life. However, the thought of buying a property may seem like a far-off dream, especially for average income earners. To own a home, you’ll need to make a down payment, which is usually 20% of the entire home price. This is usually the greatest hurdle for first-time homebuyers. Nevertheless, it’s never impossible, especially with effective financial planning.

Here are six practical tips to start saving for your first home:

1. Build a realistic budget and financial goal

When saving for your dream home, always determine your price range. Setting a financial goal will support your decision to buy a house and encourage you to commit to specific milestones. Having a realistic budget will also prevent you from going into the homebuying process blind to the costs. Additionally, this will help you determine how much money you’re saving and what you’re saving on.

Always remember that buying a home is a huge financial commitment. To set a realistic budget, figure out what type of house you plan to buy, how much monthly mortgage you can afford, and how much down payment you’ll need. You also need to estimate other fees, such as closing costs, taxes, maintenance, and insurance.

Aside from the home sale price, here are other fees that you need to consider in your budget:

- Down payment: 5 to 20% of the home sale price

- Closing costs: 2 to 5% of the home sale price

- Moving expenses: depending on your location

Pro tip: You don’t have to save for the entire amount of the house before buying it. If you’re planning to mortgage a home, most lenders recommend saving at least 20% of the home price to pay for the down payment. Though it’s not always necessary to save that much, not having a strong down payment might cost you more money over the lifetime of your home loan.

2. Set a monthly savings plan

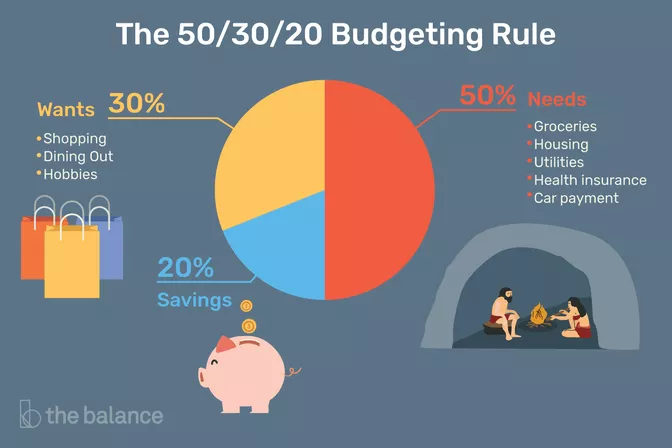

Once you’ve set a realistic housing budget, the next step is to commit to a monthly savings plan. If you’re not sure how much of your paycheck should go to your savings, follow the 50/30/20 rule. This rule suggests that 50% of your after-tax monthly income should go to your needs, 30% to your wants, and 20% to your savings.

Your needs should include your monthly rent, utilities, transportation, groceries, healthcare, and minimum loan repayments (if any). Your wants may include dining out, shopping, holidays, gym membership, and monthly entertainment subscriptions. Once you’ve covered your basic needs, always stash away at least 20% of your monthly income for savings. By saving consistently per month, you build a more durable and achievable savings plan.

Pro-tip: To visualize where you’re putting your money each month, always track your expenses and categorize them in a spreadsheet. You can evaluate and adjust your monthly spending to match your savings plan.

3. Consider downsizing

If you want to save up faster, cut down on some of the luxuries that you could live without. Always be wary of costly expenses such as expensive vacations, fancy dinners, high-end clothes, monthly subscriptions you don’t actually need, etc.

You can also cut down on some routine expenses and consider downsizing. For instance, you might want to get a cheaper phone plan, look for a cheaper apartment, or jog around your neighborhood instead of paying for a monthly gym membership.

Pro-tip: Re-evaluate your monthly bills and find ways to lower your utility costs. For example, always turn off unused appliances and lights at home, check your water line for any leaks, and be mindful of your grocery shopping routine to prevent food waste at home. Instead of throwing your cash in the trash, funnel them directly into your savings account.

4. Minimize or ditch unhealthy habits

To save more effectively, you need to drop bad money habits and build good personal finance. Bad money habits that seem trivial can set you up for failure and prevent you from reaching your housing goals. Examples of these habits are not budgeting, spending more than you earn, living paycheck to paycheck, and (you guessed it) not saving enough for your long-term goals and unexpected emergencies.

You can also save more money if you minimize or completely remove unhealthy habits. These personal habits not only hurt your health but also your wallet, which could hinder you from achieving true financial freedom. Some of the unhealthy habits that are costing you money include smoking, drinking alcohol, gambling, fast food, and too much caffeine.

Pro-tip: If quitting your bad habit altogether is difficult, your first goal should be to get your habit down to a reasonable level. The key is to practice moderation. You should also be open to new alternatives that can save you more money and make you healthier. For example, instead of going to Starbucks every so often to keep you awake, why not invest in more quality sleep?

5. Look for a side hustle

If you’re not very keen on downsizing, consider looking for a side hustle that can fund your first home. Instead of feeling bad about not going to the gym, you can increase your income. With the booming gig economy, finding an online or offline side job has become much easier and faster.

If you have the right skills and the time to spare, you can earn some extra cash by becoming an Uber driver, delivering food or groceries in your neighborhood, or becoming a photographer. You could also look into online tutoring, resell some of your pre-loved items, babysit, clean houses, rent out a spare room, or even start your Youtube vlog.

By earning an additional income, you can put more money into your housing fund and buy your first home faster.

6. Minimize your debt

Buying a home is a long-term financial commitment and having a lot of unpaid debts might make it unbearable for you in the long run. If you plan to mortgage a house, the last thing you want is to drown in more debt. Before adding new debt, work towards minimizing what you currently owe.

You can start by paying off debts with high-interest rates and fees. This will reduce the total amount of money you owe over time. If you have multiple credit cards, consider retaining only a few with the lowest rates available to manage your debt. You can also contact your creditors about setting up a repayment plan that is more realistic for your budget and can reduce your monthly dues.

Bottom Line

One of the greatest joys in life is owning and living in your dream house. Yet saving for your first home could be a challenge. The trick is to take one step at a time and commit to a monthly savings plan. To recap, here are six tips to help you save for your first home.

- Build a realistic budget and financial goal

- Commit to a monthly savings plan

- Consider downsizing

- Minimize or ditch unhealthy habits

- Look for a side hustle

- Minimize your debt

About Ziba Property

Are you looking to buy your first house, condo, or apartment? Check out Ziba Property and search for the best residential properties online.

Ziba Property is a property listing app that connects you to property managers, landlords, and real estate agents. To learn more about Ziba Property, click here or download the app on Play Store and App Store.